+1 727 756 1632

+1 727 756 1632 reachus@velan-bookkeeping.com

reachus@velan-bookkeeping.comPosted by: Pramod

June 12, 2026

Category: Accounting

Quick Summary A Cloud-based accounting software best suited for small and mid-size companies, providing real-time financial insight, AI-driven automation, and seamless integration options is QuickBooks Online (QBO). It is high time you shift to QuickBooks Online from the deprecated QuickBooks Desktop. Outsourcing the QuickBooks bookkeeping service to a professional who is certified further saves time, Continue More

Posted by: Pramod

May 15, 2026

Category: Accounting

Every business needs to be informed about financial management, and one of the most common accounting systems is accrual accounting. This approach considers the revenues to have been earned and the expenses to have been incurred at the time they are recorded, rather than when cash is received or paid out. It provides businesses with Continue More

Posted by: Pramod

March 18, 2026

Category: Accounting

The key to business success lies in being able to manage your finances effectively. However, selecting the right cloud-based accounting software for small businesses will ultimately be the determining factor of this success. As we approach 2026, many companies will be transitioning to more flexible digital solutions that provide automatic and real-time financial information. This Continue More

Posted by: Pramod

March 14, 2026

Category: Accounting

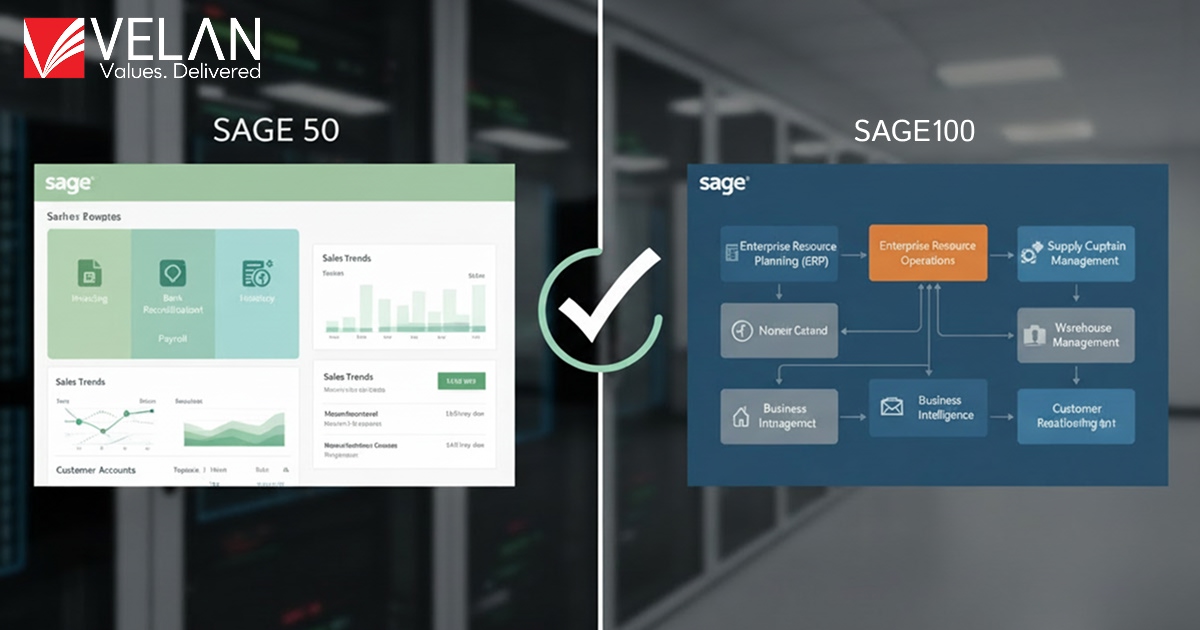

When companies are searching for accounting software which they can rely on, they oftentimes compare 2 products, which are Sage 50 Accounting and Sage 100 ERP (Enterprise Resource Planning software). They share similar use cases, as both solutions are built by Sage Group and designed to provide businesses with features to manage finances, inventory, and Continue More

Posted by: Pramod

March 03, 2026

Category: Accounting

Managing business finances in the traditional sense can involve tedious manual bookkeeping and the use of error-prone spreadsheets. The owners of businesses require efficient daily business accounting, access, and live data. This is where Sage Business Cloud Accounting comes into it. It is a cloud-native, secure, cloud-based accounting solution purpose-built for small and medium businesses Continue More